What Is UBIT and How Does It Affect Self-Directed IRA Investments?

I recently spoke with a Self-directed IRA investor who expressed concern about UBIT. They seemed to not be able to get over their “analysis paralysis” of putting their investment dollars to work for fear of what this tax could potentially do to their returns.

So, in good faith, I have decided to write up a brief article describing UBIT and how investors can confidently invest in Real Estate using their Self-directed IRA, all while NOT being concerned about UBIT.

UBIT is a hefty tax that can penalize up to 37% of your investment account on business income!

There must be two hurdles that your SDIRA investment must overcome to be exempt from paying UBIT.

First hurdle:

Is the income passive?

I know that you may have heard a sponsor or GP claim that their investment is passive, that you, as an investor, do not have to “do anything,” i.e., passive.

While that may be true of your personal time, energy, or effort, UBIT does not consider you; it considers the SDIRA. Is the invested capital “doing anything”? That’s the question.

The second hurdle:

Is the investment utilizing leverage, i.e., debt, on the assets it is acquiring?

While, in theory, many syndication investors may be able to argue that, yes, their capital is passive (I will show you that this is not the case when investing in syndication), it is very hard to get over the second hurdle. Almost every single syndication utilizes debt, and many funds utilize debt as well.

I want to address each of these hurdles as well as reveal an exemplary way to truly passively invest in real estate while being able to walk over both of these hurdles seamlessly.

"I am not a tax professional nor a Self-Directed IRA Custodian. This article does not constitute tax advice or investment advice. Please consult with your Self-Directed IRA custodian for more details concerning UBIT and how it may affect your retirement accounts.”

What is UBIT

UBIT, or Unrelated Business Income Tax, refers to a tax imposed on income generated from a business activity that is not substantially related to the tax-exempt purpose of an organization, such as an IRA.

When a Self-Directed IRA (SDIRA) engages in certain business activities, it can trigger UBIT. UBIT can be triggered by two primary events within your investment of choice and can significantly affect your expected earnings.

SDIRA investors may find themselves facing UBIT if one of the following is realized: Business Activities, which is hurdle one, or Debt Financed Income, which is hurdle 2.

For most of you who use your SDIRA to invest in real estate, the first event MAY apply, which I will cover in the next section.

However, the second event is definitely more common, which I will cover in section 2. In either regard, it’s wise to be strategic about where and how you utilize your SDIRA to invest in real estate.

After sharing these two UBIT Triggers, I will share the methodology of investing in real estate, which I believe is superior to buying real estate inside your SDIRA.

Combining a specific vehicle and a specific methodology I am confident that you as a passive investor, desiring to diversify into passive cash-flowing assets in real estate through your SDIRA, will be excited to explore this methodology using your SDIRA.

Business Activities UBIT

If the SDIRA invests in an active business (like a partnership or an LLC) that generates income, that income may be subject to UBIT. This can happen if the IRA invests in businesses that are considered to operate as active trade or business rather than passive investments (like stocks or bonds).

The investor I was speaking with was faced with this scenario. They had invested in a syndication as an LP (a passive investor).

They were not doing any work to the property. The Sponsor and their team handled the acquisition, renovation, and disposition of the assets, and they were happy to collect the profits once the properties sold. BUT THEN….

The time came to start selling the assets. The Sponsors did a great job of turning the properties around and increasing the market value.

They were able to sell the properties at a significant value!

All the LPs were very happy after just 2 years, and they were anticipating getting paid back their investment plus their return…. that is, everyone except this investor.

Because they had invested in a Fix & Flip fund, the profits generated from the sale of the assets, thus capital gains, failed to clear the first hurdle.

You see, UBIT is due when the fund or syndication is fixing & flipping properties or involved in new construction or development.

Because the income generated from the sale of these properties hit this hurdle smack dab in the center, the investor was facing a 37% tax on the business income generated from the sale of the asset.

More of a consideration, though, is how these Fix & Flip Funds, Reposition Syndications (what you call an MF or Commercial acquisition/ improvement/ and then refinance), and New Construction type of funds leverage debt to help the funds raised dollars go further.

This assumption of debt is what most often triggers UBIT and what I will cover in the next section.

Debt Financed Income UBIT

The approach to using debt (leverage) by real estate investors is not only acceptable to grow wealth, its wise and strategic positioning generate much higher returns than using only cash.

Of course using only cash almost eliminates the “threat” of loosing the asset due to not paying obligatory payments (taxes are always required, even on a free and clear property). This assumption of debt by equity funds is a double edged sword.

To best understand debt-financed income as it relates to UBIT, let us consider the following example:

You are a passive investor, an LP, in an MF Syndication.

The Syndication Sponsor plans on purchasing the asset with a 70% LTV loan and is raising 30% of the DP + the OpEx “Operational Expenses” for the first year of operations, as the property will not cashflow enough to cover all expenses.

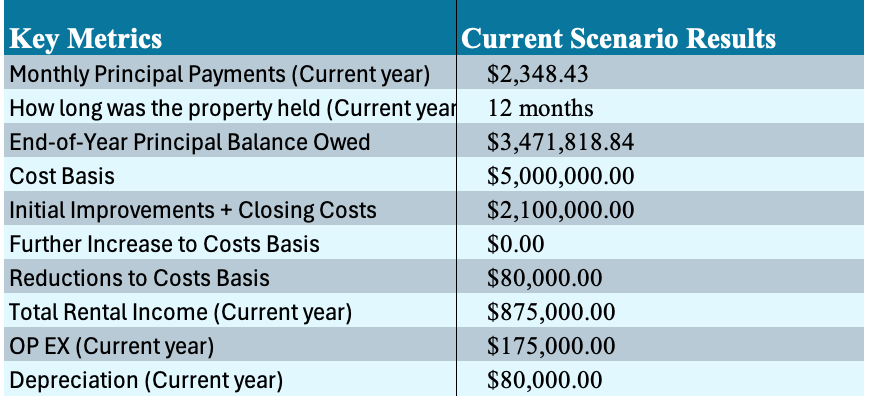

Let's assume the MF acquisition cost is $5M; thus, $3.5M will be financed. The sponsor is raising $1.5M in equity (ie, down payment), and they want to raise another $2.1M for Construction + OpEx.

The LP “Limited Partner” minimum investment is $50K; thus, around 73 investors are allowed in at the minimum investment amount.

The Waterfall is an 80/20 profit split. The ARV “After Repair Value,” once fully leased at the improved market rents, will be $11M, with a CAP rate of 6%.

In this example, the Annual cash flow equals $875K, with a vacancy rate of 5% and OpEx of 18% (this includes management company fees, HOA/ Condo Fees, maintenance, etc.).

There is no other income, so our NOI is $700K. Based on a 6% Cap Rate, our value is right at $11M.

We still have to pay annual taxes, insurance, Sponsor management, and our debt service out of that NOI. Let’s say that the NET annual cash flow equals $425K. This means that every investor (73 of them) will receive about $5,800 per year for their $50K investment, which means they will get 11.6% annual return.

So what is the UBIT exposure to an investor who invested $50K?

First off, if earned income, incurring UBIT, is LESS than $1,000, then those earnings are exempt.

Unrelated business taxable income (UBTI) generated by an asset is significantly connected to the amount of debt associated with it.

The calculation of income is considered UBTI, which involves multiplying the asset’s income by a specific fraction. This fraction consists of two components: the numerator, which is the average acquisition indebtedness, and the denominator, which is the average adjusted basis of the debt-financed asset.

The average acquisition indebtedness represents the average amount of debt incurred to acquire the asset, while the average adjusted basis reflects the asset's value adjusted for factors such as depreciation or appreciation over time.

This fractional calculation is essential because it determines the portion of the asset's income that will be subject to UBTI tax.

It’s important to note that when an asset is sold or otherwise disposed of, the debt used in the numerator for this fraction is not the current outstanding amount but rather the highest amount of outstanding debt that was recorded during the previous 12-month period.

This approach ensures that the UBTI calculation reflects the peak leverage point of the asset, providing a comprehensive view of the debt's impact on calculating UBTI.

Now, out of the $5,800, the investor also received depreciation, which reduced their earnings to $4,688.89.

There are a lot of factors that I simply don’t have the time to get into, but here is a short list of key metrics you/ your sponsor should be aware of when calculating UBIT:

So using this information, the total amount of UBIT paid by the Sponsor is $46,233.00. Thus, the cost passed onto each of the 72 investors equals $$642.13.

*This is a complete assumption, and your CPA will be able to account for what you specifically owe accurately. THIS IS ONLY FOR DEMONSTRATION PURPOSES ONLY!

So now let’s look at what the EOY profit actually was and extrapolate your annualized return. Due to depreciation, you now have $4,688.89, less the UBIT Tax you now must pay you are left with a profit of $4,046.76.

This equates to an annualized return of 8.093%. Not bad, you have historically beat out the S&P 500. However, your annualized return was reduced from 11.6% to 8.09%… that’s almost a 3% reduction in annualized returns!

A BETTER Way to Invest Your SDIRA

So here is the ULTIMATE question and need of every investor who uses or is interested in using an SDIRA to invest in real estate… “How can I INCREASE my annual return while eliminating UBIT?”

I’m glad you asked!

There is a way that passive investor cn increase their yield while mitigating tax consequences. By using their SDIRA to invest in debt.

Yes, thats right, by investing in debt. Isn’t debt bad? Well, if you follow Dave Ramsey, you may be inclined to think so, but even Dave is hyper-focused on eliminating the assumption of debt, meaning debt that you, as a consumer, take on.

But investing in debt is an excellent way to be smart and sophisticated with your investments, stay in control of assets, mitigate your risks, and significantly increase your annualized return using your SDIRA, which by nature is created as a tax shelter… why would anyone willingly incur taxes onto a tax shelter vehicle!?

Don’t be like the millions of SDIRA investors across the US who make this mistake!

When you invest in debt, you are thinking, analyzing, and investing just like banks do by becoming lenders. When you are the bank, even with an SDIRA, you receive dependable, regular monthly payments via the loan you gave, and that loan is secured to the asset you loaned on!

Think about the scenario above. If you were the bank, you would have had a loan of only $3.5M secured to an asset worth $11M… thats over $7.5M in equity thats yours if the borrower defaults!

Believe me, the borrower has a lot of incentive to make your monthly payments.

“But Edwin, I don’t have $3.5M in my SDIRA! How in the world can I participate on the lending side when I only have $50, $100K, or even $500K in my SDIRA?”

This is a valid and frustrating question, but… I have a solution.

Blue Bay Fund I accepts Accredited investors who use their SDIRA to invest in funds. Our fund does not utilize leverage, meaning we do not borrow or leverage the cash we have available in the fund to be able to invest more.

This we eliminate Trigger 2 from the UBIT equation. We also do not invest INTO other businesses as equity. Therefore, we eliminate Trigger 1.

We are a private debt fund, and our vehicle of choice for our investors is short-term loans secured to investment real estate. We always make sure there is protective equity in a deal, and our investors receive monthly interest income!

If you are interested in looking at ways to diversify your SDIRA into real estate investment property loans, then let's talk.

You can schedule a call with me, Edwin Epperson, by clicking on the link below, or you can schedule a time to view my presentation over Blue Bay Fund I and my data room.

I look forward to helping you make wiser, more informed decisions and expand the horizons that you can access through sophisticated investments.

With Honor,

Edwin D Epperson III,

Manager & CEO

Soli Deo Gloria